April 20, 2026

Echo45 Advisors Investment Committee

For many households, a home represents not only where they live and raise their family, but also their largest financial asset, monthly expense, and source of debt. From a broader economic perspective, the housing market is deeply intertwined with consumer confidence and economic growth. So, while investor attention has been on geopolitics and market volatility this year, the fact that home prices remain near all-time highs continues to play an important role in financial planning.

Housing activity is mixed but prices remain near record levels

Housing activity has been mixed in recent years across a number of measures. For new buyers, the biggest challenge with affordability is mortgage rates. The 30-year fixed mortgage rate is around 6.3%, well above the lows of 3% or less in 2020 and 2021, and the average of 4.6% since 2008. This means that the monthly cost of purchasing a home is significantly higher than it was just a few years ago, even for buyers with substantial down payments.

For those homeowners who were able to lock in mortgage rates near historic lows over the past decade, it can be a difficult decision to sell and give up these rates. This has kept the supply of existing homes limited, leading to a tighter housing market. In March, the sales volume of existing homes fell 3.6%, a reversal to its low one year ago, after climbing earlier this year.

In reaction to this, new construction has increased, with housing starts accelerating to 1.5 million units per year in January, but it will take time for this to ease pressure on prices. Even among homebuilders, however, the outlook remains uncertain. The NAHB/Wells Fargo Housing Market Index, which measures sentiment among homebuilders, fell from 38 to 34 in April. From a stock market perspective, the homebuilding subindustry within the S&P 500 index has been roughly flat on the year with a gain of only 0.4%, after several years of mixed performance.

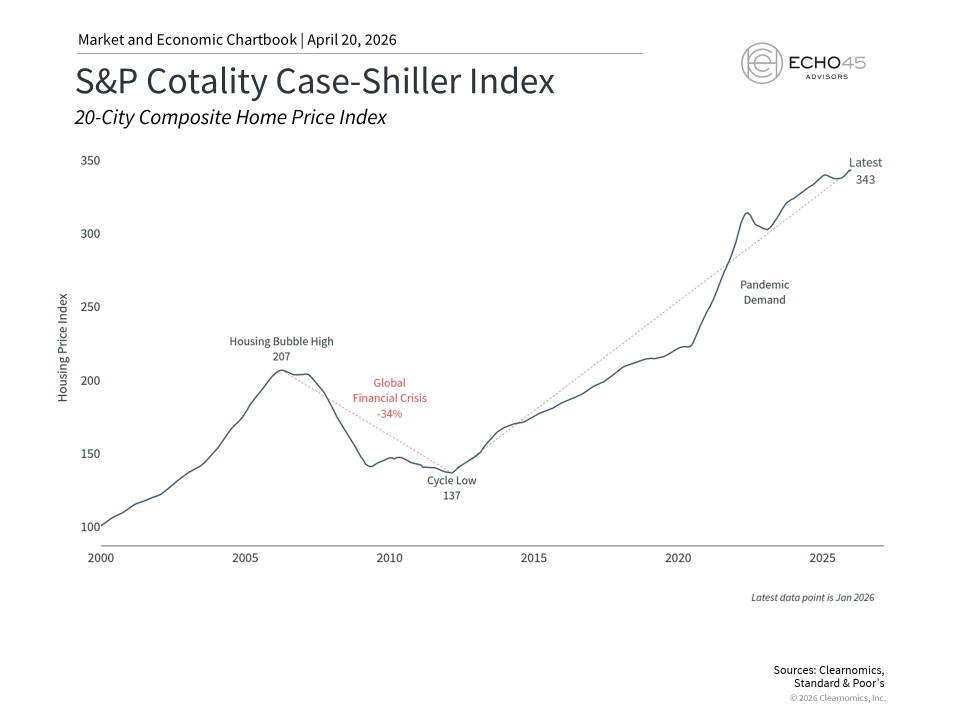

Despite these challenges with housing activity, home prices are still near record levels across the country. The S&P Cotality Case-Shiller indices, which measure prices nationally and across the largest U.S. cities, have climbed steadily. Across the country, home prices have experienced significant declines in only two periods in recent history: the 2008 housing bust and the brief pullback that followed the rapid rise in inflation beginning in 2022.

Higher home prices mean that, from a macroeconomic perspective, balance sheets for homeowners have generally remained healthy. This has been further supported by a low unemployment rate and strong wage gains, and are important reasons that overall consumer spending has held up better than many feared. These factors have helped to offset poor consumer sentiment driven by inflation and job losses in certain sectors, such as in tech.

Housing is often the foundation of wealth across generations

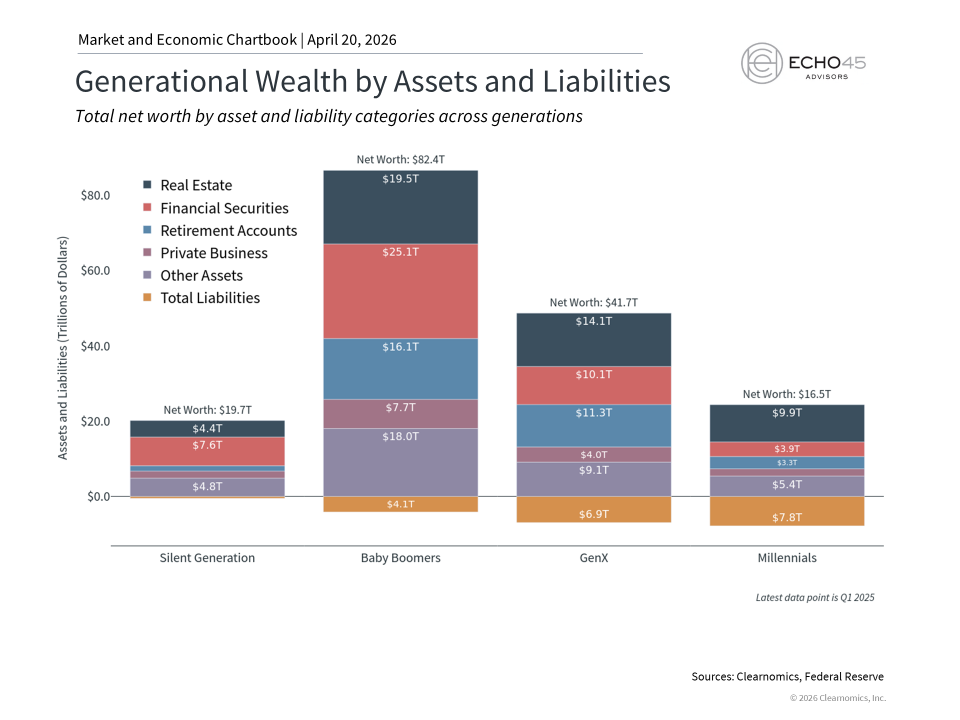

As the chart above illustrates, real estate is an important component of household net worth across all generations. For older Americans, real estate holdings often represent a significant share of total assets accumulated over decades. Baby Boomers, for instance, hold over $19.5 trillion in real estate, representing roughly 24% of their total net worth. For Gen X and Millennials, that share rises to approximately 34% and 60%, respectively. Of course, real estate is also a significant source of outstanding debt for younger households that have not had time to pay off their mortgages or benefit from decades of housing market growth.

This “wealth effect” is important, especially when the stock market is volatile and the world feels uncertain. When home values rise, homeowners tend to feel more financially secure and may be more willing to spend on goods and services, supporting broader economic growth. They may feel this way even if they do not actively access their home equity, such as through a reverse mortgage or home equity line of credit.

This also highlights the importance of maintaining a holistic perspective around financial planning. This is because short-term stock market swings, while never pleasant, may be less impactful to an investor’s financial picture than they may perceive, since much of their wealth is tied to other assets. In fact, depending on the investor’s specific situation, prioritizing mortgages and other forms of debt may be more helpful than focusing on the stock market.

These psychological and financial effects make the housing market important as both an economic indicator and when it comes to financial planning. Inflation is another factor that is affected by housing costs, since it is the primary driver of the “shelter” category within the Consumer Price Index. Even before energy prices led to the latest jump in headline inflation, elevated shelter costs were an important reason that inflation has been slower to return to the Fed’s 2% target.

Household debt levels reflect both mortgage and consumer borrowing

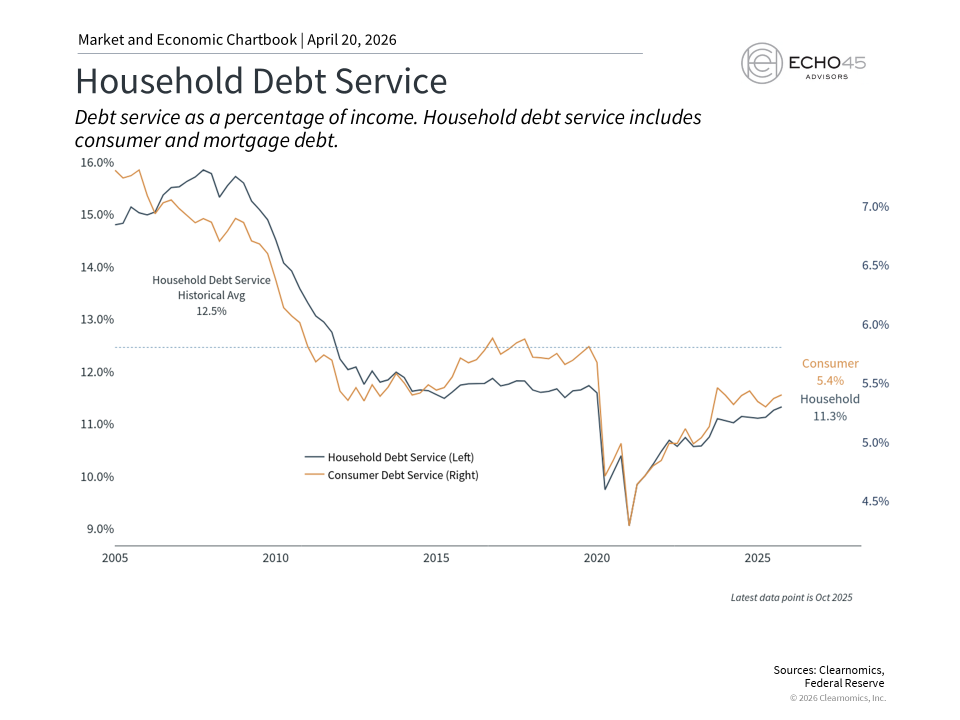

Of course, housing is not only the largest asset on most household balance sheets, but also the largest source of debt. The accompanying chart shows both household debt, which includes mortgages, and consumer debt, which does not. Even as other forms of debt rise, including credit cards and student loans, mortgage debt represents by far the largest component of total household borrowing.

One encouraging aspect of today’s environment is that debt service levels (the size of debt payments relative to household income) are still moderate relative to history. Mortgage underwriting standards have also been considerably more conservative since the 2008 financial crisis, when household debt levels were far higher. Still, the burden of these debt payments is a real consideration for many households, particularly those who purchased homes in recent years at higher prices and interest rates.

So, from an economic perspective, healthy home prices could continue to support consumer balance sheets and the broader economy despite mixed activity. From a financial planning perspective, it’s important for investors to have a clear understanding of their full financial picture. While headlines have focused on stock market swings and the Middle East conflict, the truth is that focusing on aspects of our financial plans closer to home may play a much larger role in achieving long-term goals.

The bottom line? The housing market remains a core part of both household finances and the broader economy. With ongoing market volatility, understanding the key drivers of household wealth can help investors maintain perspective and stay focused on their long-term financial plans.

Echo45 Advisors LLC is a Registered Investment Advisor. Registration does not imply any level of skill or training. The information and statistics in this report has been obtained from Clearnomics, a separate and unaffiliated organization. Based on our own due diligence, we believe Clearnomics to be reliable but we do not warrant their accuracy or completeness. This report is for your information only and does not constitute an offer to buy or sell, or the solicitation of any offer to buy or sell any securities. Advisory services are only offered to clients or prospective clients where Echo45 Advisors LLC and its representatives are properly licensed or exempt from licensure. Past performance is no guarantee of future returns. Investing involves risk and possible loss of principal capital. No advice may be rendered by Echo45 Advisors LLC unless a client service agreement is in place.

© 2026 Clearnomics, Inc. All rights reserved. The information contained herein has been obtained from sources believed to be reliable, but is not necessarily complete and its accuracy cannot be guaranteed. No representation or warranty, express or implied, is made as to the fairness, accuracy, completeness, or correctness of the information and opinions contained herein. The views and the other information provided are subject to change without notice. All reports posted on or via www.clearnomics.com or any affiliated websites, applications, or services are issued without regard to the specific investment objectives, financial situation, or particular needs of any specific recipient and are not to be construed as a solicitation or an offer to buy or sell any securities or related financial instruments. Past performance is not necessarily a guide to future results. Company fundamentals and earnings may be mentioned occasionally, but should not be construed as a recommendation to buy, sell, or hold the company’s stock. Predictions, forecasts, and estimates for any and all markets should not be construed as recommendations to buy, sell, or hold any security--including mutual funds, futures contracts, and exchange traded funds, or any similar instruments. The text, images, and other materials contained or displayed in this report are proprietary to Clearnomics, Inc. and constitute valuable intellectual property. All unauthorized reproduction or other use of material from Clearnomics, Inc. shall be deemed willful infringement(s) of this copyright and other proprietary and intellectual property rights, including but not limited to, rights of privacy. Clearnomics, Inc. expressly reserves all rights in connection with its intellectual property, including without limitation the right to block the transfer of its products and services and/or to track usage thereof, through electronic tracking technology, and all other lawful means, now known or hereafter devised. Clearnomics, Inc. reserves the right, without further notice, to pursue to the fullest extent allowed by the law any and all criminal and civil remedies for the violation of its rights.