June 22, 2026

Echo45 Advisors Investment Committee

Alan Greenspan once said "since I've become a central banker, I have learned to mumble with great incoherence." Greenspan, who passed away recently at the age of 100, served as the Chair of the Federal Reserve from 1987 to 2006 and became one of the most influential economic figures of the 20th century.[1] As we reflect on his legacy just days after Kevin Warsh chaired his first Fed meeting, the parallels between the two leaders highlight several changes in how the Fed might operate in the coming years.

Connecting the Fed’s past with its future is helpful to understand how investors should view monetary policy going forward. Greenspan leaves a complex legacy bookended by a long period of stability after the inflation of the 1970s and early 1980s on the one hand, and the housing bubble and global financial crisis on the other. Throughout this timeline, it’s undeniable that he helped to define the role that the Fed still plays today.

Perhaps it’s not a coincidence that Warsh's vision for the Fed echoes parts of Greenspan's era, which favored less explicit communication, fewer policy hints or “forward guidance,” a smaller balance sheet, and a narrower focus on its core mandates. At the same time, it’s important to remember that the economy and markets have grown under different leaders at the Fed. This is because the Fed does not control many of the underlying drivers of the economy, such as technological innovation and demographic trends. How should long-term investors view the latest changes at the Fed while keeping its history in mind?

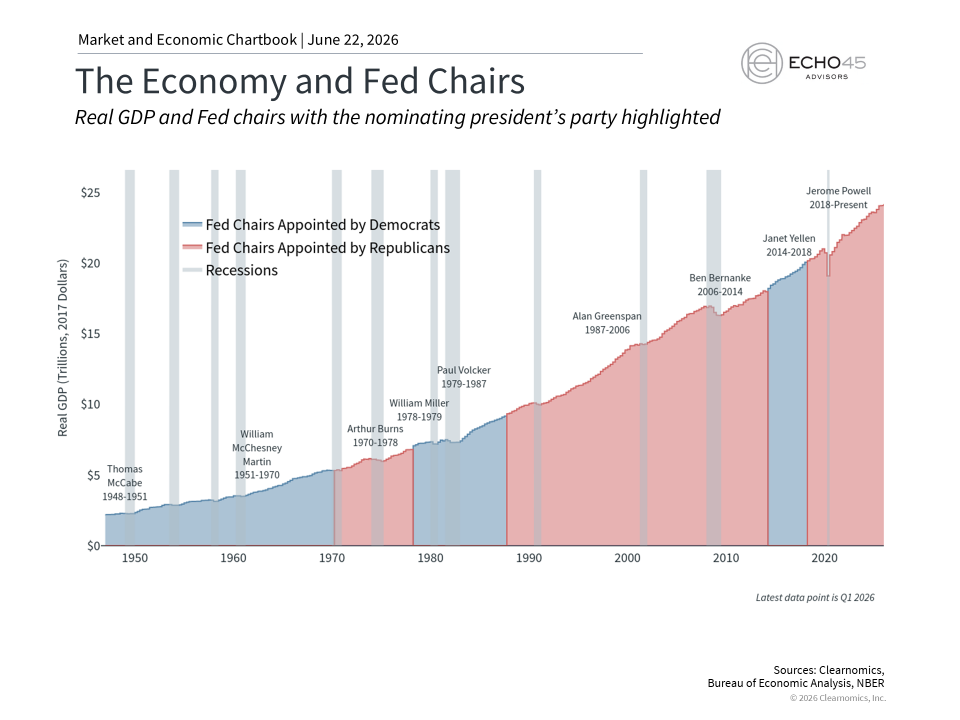

The economy has grown across many Fed chairs

It’s important to remember that the Fed has not always operated the way it does today. For much of Greenspan's tenure, the central bank did not even announce its rate decisions publicly. Instead, the Fed effectively operated in secrecy, and markets were left to infer what had happened by watching short-term rates in money markets. When it did issue communications, the language was difficult to understand, something that economists refer to as “Fedspeak.”

It was not until 1994 that Greenspan introduced the practice of issuing a statement when rates changed, and even then, the statement was extremely brief with little explanation.[2] As this practice started to take hold, the Fed started including language that partly explained its decision-making process based on the economic environment.

This continued to evolve over the next three decades. The Fed’s modern use of press conferences, dot plots, and forward guidance were developed under Ben Bernanke, Janet Yellen, and Jerome Powell. Many of these policies were driven by economic crises, including in 2008 and 2020, during which the Fed believed that communication was an important tool for restoring confidence in the financial system.

Despite the many differing views on how the Fed ought to operate, the accompanying chart shows that the U.S. economy has grown across the tenures of many different Fed chairs, nominated by presidents of both parties. These Fed leaders each navigated unique economic challenges and set up the playbook for their successors. The economy continued to expand over long periods despite different approaches to monetary policy and different relationships with the White House.

Warsh's approach marks a shift in communication

While the purpose of these communication changes was also to enhance transparency around how the Fed operates, Warsh and others have argued that the pendulum has swung too far in that direction. So, at his first FOMC meeting in June, Warsh made several changes. The Fed statement was significantly shortened, removing much of the language that has become boilerplate.[3] Any “forward guidance,” meaning the practice of signaling what the Fed might do at future meetings, was removed. Warsh also declined to submit his own forecasts to the FOMC's Summary of Economic Projections, a sign that he does not view these numbers as helpful.

Perhaps most importantly, Warsh announced five working groups to study different aspects of Fed operations and policymaking. These include communications, the data the Fed uses to assess the economy, its inflation framework, the impact of AI and technology, and the balance sheet. These are in line with Warsh’s previously published views on how the Fed should operate.

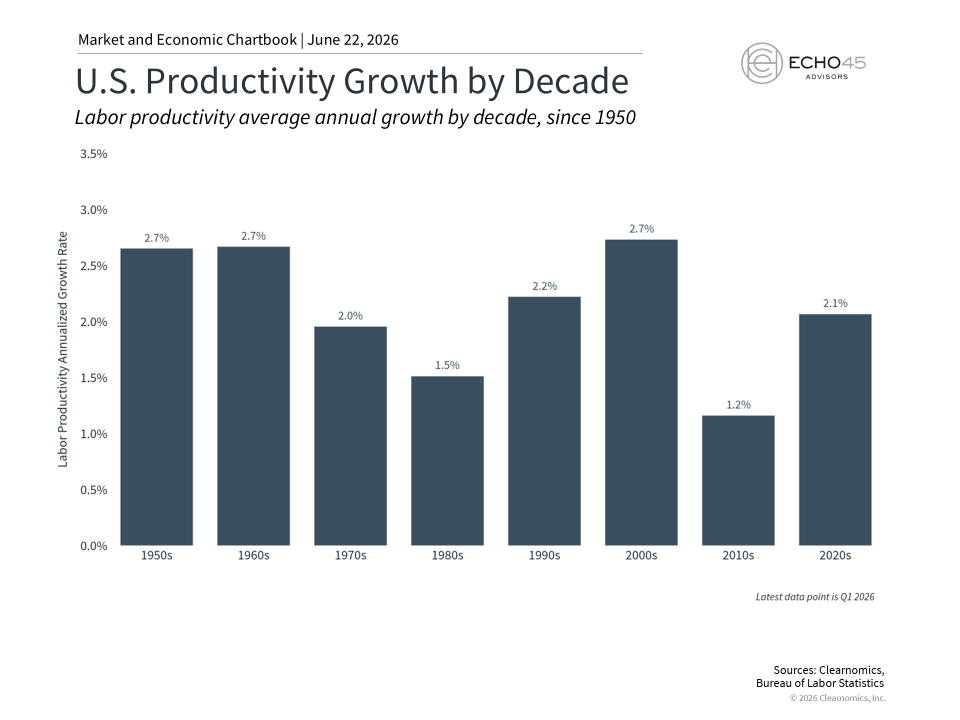

For long-term investors, perhaps the most interesting area is around productivity growth driven by AI. As the accompanying chart shows, productivity growth has been uneven across decades, with a notable acceleration during the technology-driven expansion of the 1990s. Productivity is very difficult to measure accurately in real-time, and even small changes can result in big differences to overall economic growth since they compound over time.

This matters because, in simple terms, productivity allows businesses to produce more with less labor. While much of the AI discussion is rightfully around jobs and disruption, in the long run, productivity is what allows wages and standards of living to increase. Technology can also help to keep inflation under control if it truly reduces the cost of producing goods and services.

Of course, this has significant implications for monetary policy. In the near term, the Fed has been managing a challenging period of inflation, and the ongoing war in Iran continues to create uncertainty around energy prices. The latest Fed rate projections show that the committee is divided, with roughly half expecting rates to remain at current levels by year-end and the other half expecting them to move higher.

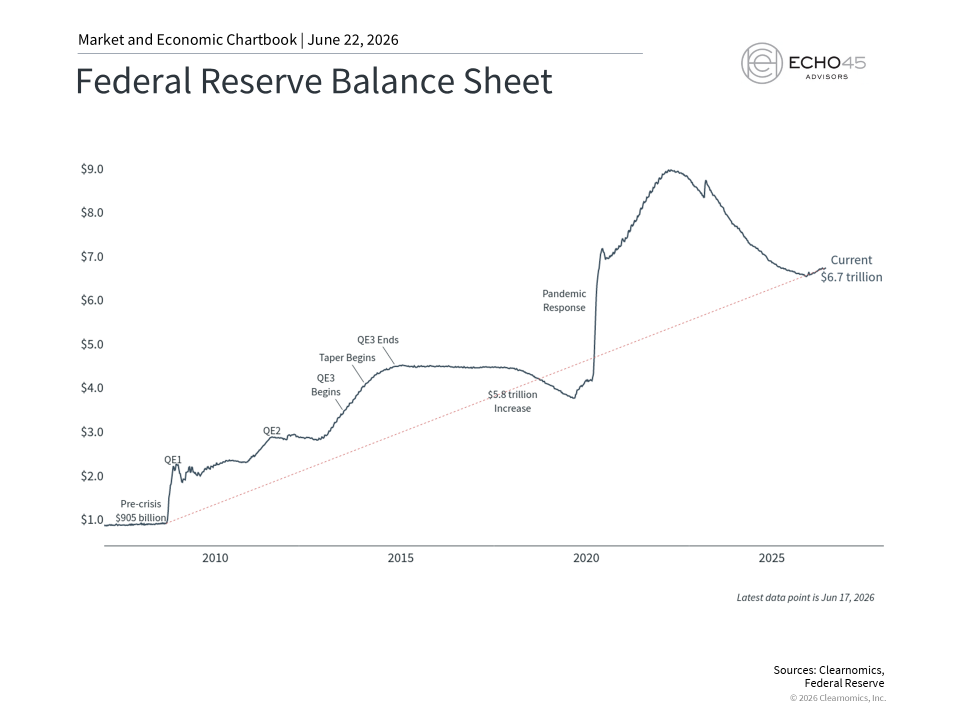

The Fed's balance sheet remains a focus

Interest rates are not the Fed’s only policy tool. As the accompanying chart shows, the Fed's balance sheet stood at less than $1 trillion before the 2008 financial crisis, then expanded dramatically through several rounds of asset purchases. In times of crisis, the Fed has directly purchased bonds on the open market, primarily Treasurys and mortgage-backed securities. This provides liquidity to the financial system, effectively lowering interest rates, which is also why the Fed is sometimes known as the “lender of last resort.” Today, the balance sheet stands at $6.7 trillion, down from its peak of nearly $9 trillion in 2022.[4]

Warsh was a Fed governor during the financial crisis and supported these balance sheet expansions as emergency measures. However, he has also argued that the Fed should have been more deliberate about reversing this trend once conditions improved. Reducing the balance sheet, often called “quantitative tightening,” involves allowing securities to mature without reinvestment or, in some cases, actively selling assets.

How the Fed will change its communications, policymaking process, and balance sheet are not yet fully clear, but it’s possible that policy changes could lead to tighter financial conditions.[5] For long-term investors, this could affect bond prices, mortgage rates, corporate borrowing costs, and more. The fact that the Fed may provide less guidance might create less fedspeak, but could also create more uncertainty as to how the Fed might react to new developments.

The broader lesson is that the Fed's approach to monetary policy is not static. It has evolved in response to economic conditions, new research, political considerations, and the judgment of individual chairs. For long-term investors, it’s important to remember that the Fed is only one part of the overall picture. The underlying trends driving the economy, many of which are positive today, are ultimately what allow portfolios to support financial plans.

The bottom line? The Fed has evolved under different leaders over the past several decades. While this context is important to understand, maintaining focus on portfolio construction and financial plans is still the best way for investors to achieve their long-term goals.

References

1. https://www.federalreserve.gov/newsevents/pressreleases/other20260622a.htm

2. https://www.federalreserve.gov/fomc/19940204default.htm

3. https://www.federalreserve.gov/newsevents/pressreleases/monetary20260617a.htm

4. https://www.federalreserve.gov/monetarypolicy/bst_recenttrends.htm

5. https://www.federalreserve.gov/mediacenter/files/FOMCpresconf20260617.pdf

Echo45 Advisors LLC is a Registered Investment Advisor. Registration does not imply any level of skill or training. The information and statistics in this report has been obtained from Clearnomics, a separate and unaffiliated organization. Based on our own due diligence, we believe Clearnomics to be reliable but we do not warrant their accuracy or completeness. This report is for your information only and does not constitute an offer to buy or sell, or the solicitation of any offer to buy or sell any securities. Advisory services are only offered to clients or prospective clients where Echo45 Advisors LLC and its representatives are properly licensed or exempt from licensure. Past performance is no guarantee of future returns. Investing involves risk and possible loss of principal capital. No advice may be rendered by Echo45 Advisors LLC unless a client service agreement is in place.

© 2026 Clearnomics, Inc. All rights reserved. The information contained herein has been obtained from sources believed to be reliable, but is not necessarily complete and its accuracy cannot be guaranteed. No representation or warranty, express or implied, is made as to the fairness, accuracy, completeness, or correctness of the information and opinions contained herein. The views and the other information provided are subject to change without notice. All reports posted on or via www.clearnomics.com or any affiliated websites, applications, or services are issued without regard to the specific investment objectives, financial situation, or particular needs of any specific recipient and are not to be construed as a solicitation or an offer to buy or sell any securities or related financial instruments. Past performance is not necessarily a guide to future results. Company fundamentals and earnings may be mentioned occasionally, but should not be construed as a recommendation to buy, sell, or hold the company’s stock. Predictions, forecasts, and estimates for any and all markets should not be construed as recommendations to buy, sell, or hold any security--including mutual funds, futures contracts, and exchange traded funds, or any similar instruments. The text, images, and other materials contained or displayed in this report are proprietary to Clearnomics, Inc. and constitute valuable intellectual property. All unauthorized reproduction or other use of material from Clearnomics, Inc. shall be deemed willful infringement(s) of this copyright and other proprietary and intellectual property rights, including but not limited to, rights of privacy. Clearnomics, Inc. expressly reserves all rights in connection with its intellectual property, including without limitation the right to block the transfer of its products and services and/or to track usage thereof, through electronic tracking technology, and all other lawful means, now known or hereafter devised. Clearnomics, Inc. reserves the right, without further notice, to pursue to the fullest extent allowed by the law any and all criminal and civil remedies for the violation of its rights.